Inflation continues soaring with no end in sight and seems to shatter 40-year highs every month.

The Fed just hiked interest rates 25 basis points for the first time in almost four years and anticipates up to seven more hikes through 2023. Interest rates could potentially hit 2.75% after two years of 0% rates, effectively ending the era of free money and cheap borrowing.

Unfortunately, 0.25% rate hikes may not be enough to douse the flames, and Fed Chair Jay Powell knows it. On March 21, he showed striking transparency in saying that the inflation outlook has deteriorated. Even if the Fed funds rate rises to 2% by the end of the year, core inflation (excluding food and energy) could still hover around 4.1%. With the central bank’s back against the wall, he may have no choice but to bump rates by 50 basis points.

“If we determine that we need to tighten beyond common measures of neutral and into a more restrictive stance, we will do that as well,” he said.

Powell’s not bluffing either. In January, activist investor Bill Ackman said hiking rates 50 basis points was the only way for the central bank to regain credibility. Goldman Sachs recently echoed this and now expects the Fed to hike rates 50 basis points in May and June.

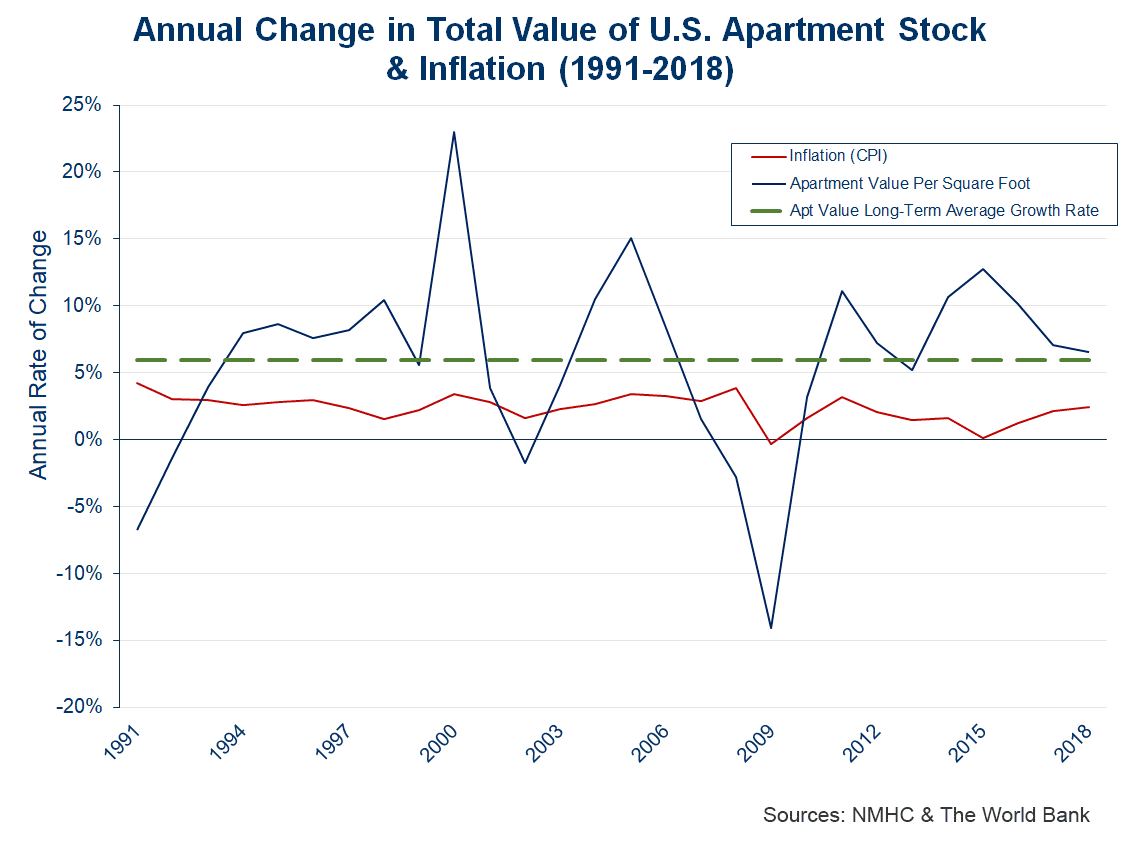

Owning physical assets in such times, such as real estate, have proven to provide a powerful portfolio hedge. To quote Russell Sage, the famous financier, “real estate is an imperishable asset, whose value keeps increasing. It is the strongest security that human ingenuity has devised. It is the basis of all security and the only indestructible security”.

Investing wisely can make all the difference. The strategies that were effective ten years ago, when inflation and interest rates were very low, may not work today.

Here are several tactics you can use to hedge against the current environment and benefit:

As mentioned above real estate is frequently regarded as one of the finest inflation hedges. This asset type has inherent value and pays out dividends on a regular basis. Regardless of the economy, there will always be a demand for homes, and as inflation rises, so will property values and rents.

Source: NMHC & The World Bank

Industrial real estate could especially be a strong bet in this environment. With the rise of e-commerce alongside supply chain issues, industrial real estate, namely warehouses and storage, should continue to rise in price and demand. Even with higher inflation, industrial real estate assets could continue providing consistent income. Moreover, industrial real estate requires less overhead and maintenance than other sectors, potentially keeping margins relatively strong even as prices and interest rates soar.

The illiquidity of real estate assets is frequently seen as their most serious flaw. This is why many investors are interested in REITs, which provide excellent real estate exposure while being significantly more liquid.

Think of a REIT (Real Estate Investment Trust) as a mutual fund or ETF for a basket of real estate properties. These companies, which commonly trade on public exchanges like a stock, own, operate, or finance income-producing real estate assets and pool together various investors’ capital. Because they trade like stocks, they are also highly liquid.

REITs are perfect for investors that don’t necessarily have Elon Musk’s capital. They mirror the consistent income streams a real estate property offers while offering convenience without requiring the immense amount of time or money you would otherwise need. Instead of paying corporate taxes, REITs pay roughly 90% of their taxable income to shareholders- which often translates into substantial monthly dividends for your portfolio.

Leveraged loans can also be an efficient inflation hedge. Their properties, such as floating rates, make them effective tools for protecting against rising interest rates. Mortgage-backed securities and collateralized debt obligations are two other viable options, since investors don’t own the debt, but rather invest in securities with loans as underlying assets.

These instruments are more complex, riskier, and frequently demand hefty initial investments. The most convenient option for most individual investors to obtain exposure to these products is to buy a mutual fund or an exchange-traded fund (ETF).

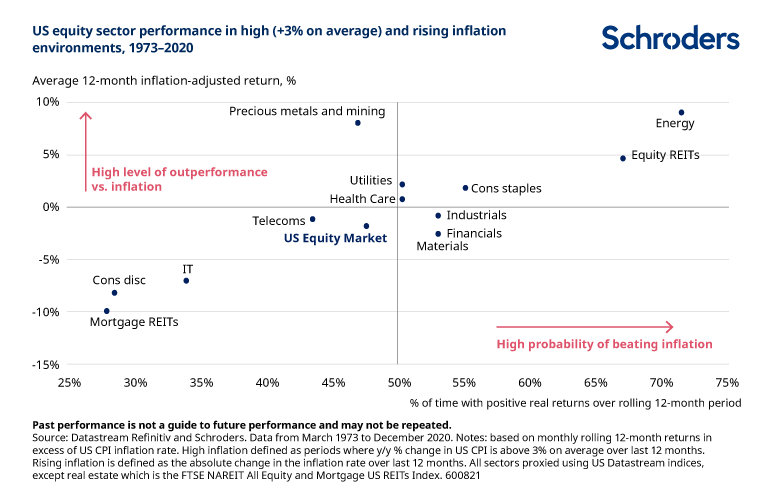

Not all stocks can keep up with inflation at the same rate. Consumer staples and energy stocks, for example, typically outperform, whereas airlines and clothes do not.

Source: Schroders

Costco is an excellent illustration of this. Since the beginning of 2022, the consumer staples retailer has had a very great performance, despite the rising inflation environment.

From an investor’s point of view, it is imperative to understand a company’s pricing power. For example – Inflation increases the price of Costco’s products; Now because people have no choice but to continue buying those products, the company continues to thrive despite inflation.

Typically, precious metals like gold and silver are where investors run to when the economic climate is uncertain or when there are wars.

Gold protects investors from inflation because it is a store of value. Perhaps that’s why Russia’s central bank resumed gold purchases massively amid the suspension of its stock market and currency collapse amid western sanctions over its Ukraine invasion.

Silver may be a cheaper alternative than gold with similar benefits and more industrial uses. According to Morgan Stanley, “Given greater industrial demand, silver tends to rise more than gold with rising inflation and a falling dollar.”

Inflation’s effect on your wallet is almost like a constant tax hike. When inflation occurs, your purchasing power declines. The dollars you earn today will not have the same value tomorrow. Rising interest rates will not help and increase the cost of borrowing.

Precious metals do not have this same problem, and we’ve seen it throughout history.

In August 2020, five months after the COVID crash, gold hit a record high of $2,067 per ounce. During the “Great Inflation” of the 70s and early 80s, when inflation hit double digits, and the Fed hiked rates to 20%, the price of gold nearly tripled in one day in 1971, surging from $42 to $120 an ounce.

On the day Russia invaded Ukraine (February 24), the price of gold soared almost as much as $100 an ounce. Weekly gold inflows for the week of March 11 were also at their highest levels since July 2020.

Over the next few years, with the economic climate murky at best, gold and silver could continue rising. You can add exposure by buying and holding the physical metal or by finding easier exposure through ETFs. Mining stocks may benefit from this environment as well.

Treasury inflation-protected securities, or TIPS, are Federally backed bonds tailor-made for inflationary times.

Unlike the structure of traditional bonds that decrease in value when yields rise, TIPS rise with inflation and decrease with deflation. TIPS bonds pay interest twice a year, at a fixed rate, and the principal and interest payments rise along with inflation.

In a nutshell, these are fixed-income instruments that protect your depleting purchasing power and correlate with inflation.

Buying physical bonds is quite pricey, and typically, those are limited to high net-worth investors. However, several TIPS mutual funds and ETFs are available that you can affordably invest in for TIPS exposure.

Everybody dislikes inflation. Nobody enjoys seeing their pricing power falter due to no fault of their own. With no end in sight and the Fed’s back against the wall, other opportunities are rising and remain plentiful. Many also remain bullish on the overall stock market and are buying in.

The above tactics might be your best bets in anticipation of persistent inflation and rising rates.

in times like this, it’s crucial to play both defense and offense, protect yourself from adverse scenarios, and hedge your bets. If you stick to your principles and remain levelheaded, you will do just fine.

The United States has entered a pivotal phase in nuclear energy development, making 2025 a critical year for nuclear energy investing. Driven by technological innovation, policy...

Remember when Bitcoin hitting $100,000 seemed like a crypto enthusiast's fever dream? Well, it just happened. On December 5th, 2024, Bitcoin crossed this historic threshold, and...

The 2025 401(k) Contribution Limits bring more than just small adjustments. While the standard limit saw a modest increase, the real headline is the enhanced catch-up...

Capital gains taxes play a key role in the U.S. tax system, applying to profits from investments like stocks, bonds, and real estate. Currently, taxes are only owed when an asset...